A social impact bond (SIB) is a contract with the public sector or governing authority, whereby it pays for better social outcomes in certain areas and passes on part of the savings achieved to investors. A social impact bond is not a “bond”, per se, since repayment and return on investment are contingent upon the achievement of desired social outcomes: if the objectives are not achieved, investors receive neither a return nor repayment of principal. SIBs are increasingly being piloted as additional funding mechanisms to existing government support for improving public health and launching new health promoting initiatives.

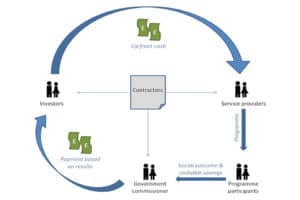

SIBs derive their name from the fact that their investors are typically those who are interested in not just the financial return on their investment, but also in its social impact. SIBs are a new mechanism providing investment to address social challenges, including health promotion and disease prevention. The mechanism can be visualised through the social impact bond diagram. In straightforward language, SIBs can be understood as a loan made by an investor, where repayment is linked to the achievement of specific agreed-upon health (or social) outcomes.

There are currently more than 120 impact bonds in 24 countries worldwide, mobilising over €330 million of investment into tackling complex social issues such as refugee employment support, loneliness among older people, rehousing and reskilling homeless youth, and diabetes prevention.

While more time is needed to make an overall evaluation of SIBs' effectiveness, in the right circumstances and developed in the right way and for the right projects, social investment bonds could be a useful tool to boost investment into innovative health promoting projects and enable public authorities to share the risk of such investment with private investors. Investments that directly improve social spaces, the lives of citizens, and improve the quality of social and health services being provided can increase the value of the social investment asset which will attract the interest of investors.

While social impact bonds are clearly an exciting new avenue to introduce innovations and improvements into the delivery and funding of health promoting services, they do not come without risks. Care must be taken that promising new funding instruments like SIBs do not result in ‘cherry picking’ or ‘creaming', which is targeting the ‘easiest’ participants or results to support to the detriment of the rest of the participants or programme. This type of perverse incentive can be avoided through careful design and service specification.

In addition, SIBs should never replace mainstream public funding and responsibilities of national, regional and local governments. However, they are well placed to pilot actions and interventions in order to demonstrate effectiveness, and secure more traditional funding for the long term and for scaling up. They can also be utilised to boost investment into health promotion and prevention measures by sharing the risk between public and private investors.

More information about Social Impact Financing is available on the Reports & Publications page.

Case studies

As a response to the global displacement crisis which peaked in 2015, the Finnish government decided to establish a social impact bond focused on the employment of immigrants. Unemployment, particularly long-term unemployment, represents a huge risk of social exclusion for immigrants; thus, finding stable and quality employment is a very important part of the integration process. The Finnish Innovation Fund Sitra proposed the idea of a SIB that would offer immigrants work-life oriented training. The subsequent three-year (2017-2019) pilot Koto-SIB for the employment of immigrants kicked off in 2015. The objective was for immigrants to enter the labour market on average four months after the training has begun. The training was followed by further on-the-job training and includes language, culture and professional skills studies.

Outcomes were measured by the following two indicators: unemployment benefits and income tax. The expectation was that the proportion of unemployment benefits paid to the people involved in Koto-SIB was smaller and that they would contribute with greater income taxes in contrast to the control group not involved in the programme. The service providers were first paid based on direct operations costs, but the rest of the payments were based on outcomes. This structure incentivised service providers to do their best to find suitable and quality work for every participating individual.

While this is certainly a promising initiative, it is important to note that not every immigrant is able to participate in these services, due to age, disability, or other conditions that render them incapable of participating in the labour market. This SIB must be complemented by additional services and programming to make sure no one is left behind. This includes strong measures to ensure that reliable, well paid jobs are included and that new arrivals have a voice on an oversight committee to ensure that their voices are heard throughout the process.

The Heart and Stroke Foundation of Canada launched a SIB, the Activate Programme, in 2018. This programme was developed in response to the high rate of heart diseases and stroke. Activate is a lifestyle-change programme to help people at risk of developing hypertension (one of the most important risk factors for heart diseases) to adopt healthier habits to get their blood pressure under control. This is Canada’s first health-related SIB.

The Heart and Stroke Foundation of Canada launched a SIB, the Activate Programme, in 2018. This programme was developed in response to the high rate of heart diseases and stroke. Activate is a lifestyle-change programme to help people at risk of developing hypertension (one of the most important risk factors for heart diseases) to adopt healthier habits to get their blood pressure under control. This is Canada’s first health-related SIB.

The Health and Stroke Foundation selected this instrument as it allowed them to innovate and develop their own governance structures. They approached the Centre for Impact Investing seeking help to establish this bond. The main negotiation involved establishing the rate of return on investment for investors that took place between the Foundation and the federal government. (In Canada, prevention is a responsibility of the federal government while the provinces are mandated to manage healthcare).

The Activate Program

The Activate program is a 6-months community wellness program that was designed to prevent the onset of hypertension (high blood pressure) among older adults. It is funded by a social impact bond through a pay-for-success model over the course of 3 phases from 2018 to 2020.

- The outcomes of success for the Activate program are measured by the volume of enrolments and the average change in blood pressure between recruitment and a follow-up after at least 6-months of the program.

- The target for success was set by cardiologists at no increase in blood pressure readings, but an overall decrease is even more desirable. Without intervention, half of pre-hypertensive people in Canada over age 60 will go on to develop high blood pressure within four years.

- Cohort 1 of the Activate program enrolled 527 participants into the program and we observed an average change in blood pressure of -5 mmHg systolic.

- As of Week 19 in Cohort 2, there were ~1950 enrolled new participants, and the team expanded the program beyond the initial plan of the Greater Toronto Area to include several other regions in Ontario, Canada.

Hypertension is the number one risk for stroke and leading risk factor for heart disease. Without intervention, half of all pre-hypertensive people over 60 in Canada will develop hypertension within 4 years. Heart disease & stroke are leading causes of death, taking the lives of more than 66,00 Canadians every year. This program is an opportunity to assess the impact of preventative health measures on hypertension. The target for success was set by cardiologists at no increase in blood pressure readings, but an overall decrease is even more desirable.

Funding for Activate comes from a pay-for-success (PFS) model or social impact bond (SIB). Working closely with the MaRS Centre for Impact Investing, Heart & Stroke has attracted philanthropically minded private investors to provide upfront capital. The federal government, through the Public Health Agency of Canada, repays the investors based on successful outcomes. This is only the second time in Canada that this funding model has been used, and the first time for a large-scale chronic disease prevention initiative.

Measuring outcomes

The Activate program uses two main outcome measures to determine its success. The first is volume; how many people are enrolled in the program? So far, 7000 people have been enrolled. The second outcome is blood pressure; were we able to halt the increase in blood pressure over the 6 month journey? Success was defined as a flattened blood pressure trajectory (meaning no increase). A decrease in blood pressure is seen as an over-performance.

Payment for investors

Investors get paid after the recruitment phase of each cohort based on volume, as well as a final payment based on blood pressure reading. The program entails 4 key payments:

- Volume Payment 1 - Summer 2018

- Volume Payment 2 - Summer 2019

- Volume Payment 3 - Summer 2020

- BP Payment - end of the entire program, so early 2021 if not the very end of 2020

The rate of return depends on both volume and blood pressure at the end of the program. While the funds come from the federal government, the outcome payments do not come from funds for existing for services (e.g., hospitals).

Commissioners from the health system and local authority adult social care providers in Worcestershire, England introduced a social impact bond in 2014. The different stakeholders came together and decided that the relationship between loneliness, health and service use provided a rationale for expanding services to address loneliness and social isolation in the community. The service commissioners were attracted by the SIB mechanism, under which investors fund the service up front and commissioners only pay if outcomes are achieved. The commissioners were interested to transfer some of the delivery risks in developing the programme and keen to stimulate innovation and adaptation.

The Reconnections programme

![]() The end result of this approach was the ‘Reconnections’ programme. This programme takes a tailored approach to the needs of participants. A volunteer or caseworker supports an identified person in need over a period of six to nine months to re-engage with interests and social relationships of their choice and overcome practical and emotional barriers. Since its launch in 2015, over 1,300 older people have been supported. On average, self-reported loneliness is significantly lower at 9 months and 18 months after entering the service. Early evaluations by the London School of Economics are also positive and the service has been held up as an exemplar by national policy makers on how to tackle loneliness and social exclusion in later life.

The end result of this approach was the ‘Reconnections’ programme. This programme takes a tailored approach to the needs of participants. A volunteer or caseworker supports an identified person in need over a period of six to nine months to re-engage with interests and social relationships of their choice and overcome practical and emotional barriers. Since its launch in 2015, over 1,300 older people have been supported. On average, self-reported loneliness is significantly lower at 9 months and 18 months after entering the service. Early evaluations by the London School of Economics are also positive and the service has been held up as an exemplar by national policy makers on how to tackle loneliness and social exclusion in later life.

Payment for investors

In the case of Reconnections, the social impact being sought is a reduction in loneliness. Investors receive outcome payments for each aggregate reduction in self-reported loneliness using the UCLA self-reported loneliness question (a 12-point scale).

The payment metrics used in the programme are

- = £740 (c.€850) per point reduction after 9 months after service start

- = £240 per (c. €275) (sustained) point reduction 18 months after service start.

These outcome ‘tariffs’ were set due to growing evidence on the relationship between loneliness and poor physical and mental health and consequent healthcare and social care usage. A London School of Economics interim evaluation found that reducing loneliness in people who feel lonely most of the time could potentially save up to £6,000 per person in costs to the system over 10 years.

The service costs approximately £330,000 (€380,000) each year to support up to 430 older people a year (c. £750-800 per participant). At the start of the service, investors provided £650,000 in up-front capital - £565,000 as debt and £85,000 as equity. In the first two years of running, the service was loss-making – however, as impact has grown, and 18 months payments have increased, the service is now making a small surplus.

By April 2020, commissioners are expected to have made outcome payments of around £1 million. The first £175,000 was returned to investors in early 2019 and subsequent payments are expected 2019-2021. However, it is not yet certain that investors will fully recoup all of their initial £650,000 investment given that service costs were more than originally anticipated. This is a clear risk that investors must face when deciding to invest in social impact bonds.

In 2016, France’s average unemployment rate stood at 10.1%, which was higher than the average European Union rate of 8.1%. Unemployment rates vary from region to region and are significantly higher in rural areas compared to urban areas.

This economic disparity led to social challenges for people affected by unemployment, as well as to the desertification of towns and increased financial strain on local authorities. In fact, the cost to the state is estimated at € 15 470/year/person for job seekers no longer receiving unemployment assistance. This number corresponds to the aggregate cost of the various benefits, social assistance and loss in revenue to the State attributable to each individual.

Limited access to financial services further exacerbated the issue, especially for individuals lacking capital or formal qualifications. One potential solution is the use of microcredits. In fact, assisted microcredits are acknowledged by public authorities as a factor of social and economic inclusion, job creation, social cohesion and regional development.

Intervention and financing model

In order to address the issue of job desertification in rural areas and regenerate these regions, the Association for the Rights to Economic Initiative (ADIE) launched a social impact bond to promote access to microcredit for deprived beneficiaries. The programme targeted job seekers, recipients of minimum social benefits who aspired to start their own business, and individuals who could secure employment with improved mobility. The goal was to support them to develop a business activity in remote rural areas and re-enter the labour market.

Five investors collectively provided EUR 1.3 million in funds, distributed in four instalments between July 2017 and January 2020. ADIE was responsible for delivering its services across three rural areas. Repayment to investors was contingent upon the programme's success, with the savings generated by the Ministry for the Economy and Finance being used to reimburse them.

The results and impact of the programme are evaluated using appraisal criteria. The two results-based criteria focused on: 1) providing financing and support to at least 270 beneficiaries who were unable to obtain loans, and 2) ensuring the sustainable economic integration of 172 to 320 individuals over a period of two to three years.

Key outcomes (if applicable) and associated measurements

Between 2017 and 2019, ADIE's SIB facilitated the financing and support of 500 individuals in the targeted regions (Alpes, Burgundy, Occitanie). These individuals are expected to achieve long-term re-entry into the labor market, generating over EUR 2 million in savings for the State.

ADIE estimated that for every euro invested in this programme, the local authority gains €2.38 after two years.

Publications:

In Finland, child welfare and protection services are primarily remedial, leading to interventions that are often too late, after the child has likely already suffered some kind of harm. In addition, these services are expensive, with the highest costs associated with foster care. This cost is borne by municipalities, who are responsible for the provision of child welfare services. It is estimated that removing one child from foster care results in EUR 43 000 of annual saving for municipalities. Municipalities nevertheless face financial constraints to transition from remedial to preventative approaches.

Intervention and financing model

To address this challenge, Finland launched the Children’s Welfare Social Impact Bond, also known as Lapset-SIB, in January 2019 for a period of 6 to 12 years. This SIB aims to promote the welfare of children, young people, and families across five municipalities: Helsinki, Hämeenlinna, Kemiönsaari, Lohja, and Vantaa. It also intends to reduce the harm to children and the cost of expensive remedial services. The SIB is designed to provide upfront private investment to fund novel preventative services without impacting on the funding required for remedial services in the short term. If pre-specified outcomes are achieved, the municipality should save money on the cost of remedial services. Part of this saving will then be used to repay the investment fund, with interest, which allows municipalities to pay only for successful outcomes, ensuring cost-effectiveness.

The intervention involves multiple service providers, including SOS Children’s Village and Icehearts, that deliver tailored programmes to address specific needs within each municipality. Investors contribute to the project through a private equity fund through which services are financed. As of January 2020, the fund raised a total of EUR 5 million with investment from eight Finnish organisations. The five municipalities involved in the SIB each pay for outcomes that are achieved in their programmes, with a maximum possible outcome payment of EUR 10-12 million.

Creating a single SIB structure – while having five distinct projects – enabled to make it more appealing for investors as the risk is shared across different municipalities with different approaches.

Key outcomes (if applicable) and associated measurements

The results are monitored by measuring improvement in well-being and financial savings generated for municipalities. Despite the SIB being at an early stage, wellbeing data already indicate a significant improvement in the well-being of young people and families who benefited from the support and services provided through the SIB.

Additionally, it is also apparent that the new operating model has influenced municipal service culture, procurement practices and costs, as well as the well-being of children and young people through prevention and by identifying service gaps.

So far, approximately EUR 8.5 million has been invested in interventions and approximately EUR 4 million in performance-based bonuses have been paid for effectiveness. The programme has already enrolled 600 children and young people. A longitudinal study is underway to determine the long-term cost-effectiveness of these preventive measures.

Publications

In Portugal, approximately 7,000 children and young people are institutionalised, primarily stemming from lack of parental supervision and monitoring. This institutionalisation places a significant financial burden on the Institute for Social Security, costing between €59 and €85 million annually, with a minimum monthly expense of €700 per child. The Projeto Família initiative was launched to address the root causes of institutionalisation and reduce associated costs by promoting family preservation.

Intervention and financing model

The Projeto Família was part of the first edition of Social Impact Bonds in Portugal, implemented in Porto between July 2017 and October 2020. It aims to promote the preservation within the family home of children and young people at risk of institutionalisation, through the development of parenting and relational skills and their preparation for self-sufficiency within the family home. The intervention is divided into three key stages: the signalling of children and young people at risk and signing of family agreements, an intensive six-week phase in which a Projeto Familia technician conducts weekly work sessions with the family, and a period of follow-up and potential preservation within the family home. The primary contracted outcome was to ensure that children and young people at risk remained within their family homes for at least 9 months after the intensive phase.

The project was led by the social organisation Movimento de Defesa da Vida, with a total investment of EUR 433 276 provided by the Calouste Gulbenkian Foundation and Montepio bank. The outcome payments were managed by Portugal Social Innovation, with the Institute of Social Security overseeing the project.

Key outcomes (if applicable) and associated measurements

After three years, the Projeto Família® delivered all the contracted outcomes and achieved a 91% success rate in preserving children and young people at risk within their family homes, surpassing the initially contracted outcome of 60%. Of the 180 children and young people involved, only 17 were institutionalised. As a result of this success, 99% of the initial investment was reimbursed. However, there were delays in reimbursing investors due to the demanding financial reporting requirements.

Results showed that investing in the Projeto Família® intervention may represent cost savings of more than 90% in comparison to the institutionalisation of a minor.

It is nevertheless important to note that the SIB model allowed Movimento de Defesa da Vida to focus on families with a higher probability of success, raising concerns about "cherry-picking" – an practice that is often critisised in outcome-focused incentive systems. In addition, since the outcome payer was not the public entity benefiting directly from the intervention, there was limited incentive to integrate the SIB learnings into public policy.

Despite its success, the Projeto Família ended in October 2020 due to the absence of public funding to continue operating in Porto.

Publications

Between 2001 and 2012, homelessness in France surged by 50%, affecting 143,000 people. It is believed that homelessness rates have continued to grow since then. The 2015 migrant crisis further exacerbated the situation, placing additional strain on the existing shelter infrastructure. Due to the shortage of shelters, the French government was compelled to accommodate homeless people and asylum seekers in private hotels, costing the state on average EUR 30/day compared to EUR 20/day in dedicated shelters. This emergency solution was both costly and ineffective in providing long-term social support.

Intervention and financing model

In response to these challenges, the French government partnered with various institutional investors to launch the Hémisphère Social Impact Fund in June 2017. With a duration of 11 years, this fund aims to provide dedicated shelter accommodations and social support services to homeless people and asylum seekers across France, while reducing delivery costs for the government.

The fund is one of the largest social impact bonds in Europe and brings together EUR 100 million social impact investment from seven French institutional investors and a EUR 100 million conventional bank loan from the Council of Europe Development Bank. This capital was used to purchase and renovate 62 hotels, transforming them into 6,000 units of emergency accommodation. The fund is also being used to provide social support services.

The service provider, Adona, is responsible for providing emergency accommodation and social support to homeless people and asylum seekers. It is also responsible for achieving specific social outcomes, which are measured as rate of enrolment in education of children aged 6-16 (95%), proportion of adults who have a personalised support plan (90%), rate of access to social security benefits (80%), and rate of placements into permanent accommodation (70%). The EUR 200 million investment is financed by the fixed rents of the hotels, with institutional investors receiving an additional variable rate based upon the achievement of these social outcomes.

It is interesting to note that the Hémisphère Fund differs from the original concept of SIBs as it has separated a relatively low risk portion of the project (the real estate) from a relatively higher risk portion (the achievement of social outcomes). Typically, social investors risk their capital if social outcomes are not met, making it a high-risk investment. However, in the Hémisphère Fund, the risk to investors is mitigated, as only part of the returns is contingent on the achievement of social outcomes, while the underlying capital investment is secured through fixed remuneration from the hotel rents.

Key outcomes (if applicable) and associated measurements

Annual audits by KPMG measure the fund’s performance. In its initial years, the program's performance scores were 43% in 2017 and improved to 80% in 2018, with continued progress in 2019. On the long term, the fund aims to provide 10,000 accommodation units over 10 years, with a 3% return on investment tied to the achievement of social outcomes.

The use of private capital to fund public services presented several challenges, particularly within a politically sensitive environment. Some opposed supporting asylum seekers, while others criticised the potential for private investors to profit from social services aimed at vulnerable populations. It was therefore important to showcase the long-term social benefits and value for public spending that the fund is expected to deliver.

Publications

In the United Kingdom, individuals with severe mental health conditions, learning disabilities, or autism face significant barriers to employment. As of 2021, the employment rate for individuals with mental illness was 28.8% lower than that of the general population. Additionally, only about 8% of those in contact with secondary mental health services were in paid employment, despite studies indicating that 30-50% are capable of working. Employment is crucial for mental and physical well-being, including for people with mental health conditions and disabilities.

Intervention and financing model

The Mental Health and Employment Partnership (MHEP) was launched to address these employment challenges by helping people with mental health problems into paid employment, following the evidence-based Individual Placement and Support (IPS) model. It was established in 2015 by Social Finance who helped commission 7 large IPS services across England, using the world’s first social impact bond for IPS.

MHEP received initial funding from Big Issue Invest and support from outcome funds like the Commissioning Better Outcomes Fund, Social Outcomes Fund, and the Life Chances Fund. In total, £2 million social investment was raised that could be used to pay for services. Investors are repaid when the services lead to positive job and health outcomes for the participants.

Key outcomes (if applicable) and associated measurements

In the MHEP, SIBs’ outcomes contract payments are structured around the achievement of three pre-specified, measurable outcomes: job starts (individual spends one full day in a paid competitive employment), job sustainment (individual sustains paid competitive employment for at least 13 weeks), and engagement with service (individual engages with the programme and completes the vocational profile).

By the end of 2021, in the 5 LCF sites, MHEP had supported 392 people with severe mental illness or learning disability into starting paid work, 192 into job sustainment and 1322 into engagement with the service. This means an average of one new job start for every 3 to 4 people who engaged with the programme.

The launch of the SIBs was nevertheless complicated, as it coincided with the onset of the COVID-19 pandemic and the subsequent national lockdown in the UK.

Publications

Despite a significant decrease in the number of youth offenders and their reoffending rates over the past decade, more than one-third of young offenders in England and Wales continue to reoffend.

The stigma attached to criminal records makes it difficult for young offenders to access education, training, and employment opportunities, leading to potential social exclusion. Recidivism not only threatens community safety but also presents a challenge for local authorities, as youth offenders require tailored and comprehensive support to successfully reintegrate into society and the economy.

Intervention and financing model

The Skill Mill is a social enterprise which employs young ex-offenders to work on environmental projects across the UK. Skill Mill was launched as a pilot in the northeast of England in 2013 and, given its success, was expanded across England through SIB funding.

Skill Mill offers an intensive six-month work experience programme designed to help vulnerable young people break the cycle of reoffending. The programme is innovative as it combines environmental services, real work opportunities, and youth justice. The work is commissioned by clients including local authorities, businesses, and non-profit organisations.

The Skill Mill is funded by a mix of grants, investments from private companies, and by the Life Chances Fund. The income generated consists of outcomes payment (2/3) and revenues from local clients for completing outdoor work (1/3). Skill Mill's outcome payment structure is linked to the achievement of the following six outcomes: preventing reoffending, employment and further education, programme registration, programme completion, qualification, and attendance. The reoffending rate outcome will be compared with the figures published by the Ministry of Justice in the UK.

Key outcomes (if applicable) and associated measurements

Since 2014, Skill Mill has employed 450 young people in England, of which only 33 have been reconvicted. This results in a reconviction rate of 7.3%, a significant improvement compared to the national 63% rate. This reduction in reoffending rates translates to a five times return on investment.

The reduction in reoffending can also be quantified in terms of economic and social benefits. Based on Home Office figures on the costs of crime, the saving from reduction of reoffending is estimated at around £111,000 per re-offence. When combined with the reoffending reduction impact from The Skill Mill, this equates to approximately £ 30 million in savings.

Publications

Australia, like many other countries, faces significant challenges in child protection, particularly regarding the placement of children in out-of-home care due to safety concerns. In New South Wales (NSW), there are currently over 4,000 children in living away from their parents in out-of-home care, leading to concerns about the long-term effects on children and families and highlighting a strong need for investment in reunification services.

Intervention and financing model

The New Parent Infant Network (Newpin) is an intensive family restoration programme which is delivered by Uniting Communities (a community service organisation in NSW) in partnership with the South Australian Department for Child Protection. While the programme has existed since 1998, the launch of the Newpin Social Benefit Bond (SBB) in NSW in 2013 marked a new era for the program. In fact, the SBB arrangement brought a much sharper focus on measuring impact, and a more deliberate approach to supporting families who could most benefit from the programme.

The Programme is an 18-month centre-based programme that is designed to strengthen family engagement to enable children to return to and live safely with their families. Parents are supported to work with their strengths to improve parent-child relationships and learn from their peers.

The Newpin SIB is an outcomes-based contract where private investors provide $6.5 million in capital to Uniting Communities to fund the program. Payments to Uniting Communities are based on the proportion of children reunified with their families, with repayment tied to the programme's success in achieving positive outcomes that reduce government service costs. Investors receive returns based on the programme's performance.

Key outcomes (if applicable) and associated measurements

The programme has successfully restored 59% of children to their families, a rate nearly three times higher than the 20% counterfactual restoration rate used for comparison in the SBB arrangement. Moreover, approximately 65% of children who were at risk of being removed from their families were able to remain safely at home, avoiding entry into out-of-home care.

Investors received a financial return of 10% per year.

The Newpin SIB model was replicated in two other regions in Australia. The bond in Queensland had to however be terminated only three years into the planned seven-year term due to insufficient participant numbers and unclear integration with local child protection systems. This highlights that even if a programme was well structured and funded, implementing it in a new context is never straightforward. Implementation risks therefore need to be carefully considered.

Publications

In the United Kingdom, homeless young people who are not in education, training or employment are defined as not being in priority need under the current homelessness legislation. They also face a range of barriers to securing and sustaining accommodation and employment. Due to the complexity of their needs and circumstances, existing services often fail to adequately support them. These vulnerable young people therefore need coordinated support that can holistically address their housing, educational, and employment needs.

Intervention and financing model

The Fair Chance Fund was a 3-year social impact bond programme which ran from January 2015 to December 2017. The aim was to improve accommodation, education, and employment outcomes for homeless young people aged 18-24. Seven projects were funded under the programme, and were granted flexibility in designing and implementing their own intervention approaches. Each established their own delivery model, informed by the pattern of existing provision and the specific challenges presented by local housing and employment markets. Common elements included a housing-led approach where securing accommodation was the foundation for achieving other outcomes, and the appointment of link workers who provided holistic support tailored to individual needs.

The Fair Chance Fund was funded by the Ministry of Housing, Communities and Local Government and the Cabinet Office / Department for Digital, Culture, Media and Sport. It was funded on a 100% payment by results basis, with projects being backed by social impact bonds (SIBs) following a competitive bidding process. Social investors funded project providers to set up and deliver services, recouping their investments if and when outcomes were achieved, and triggering payments against a set of specific metrics and tariffs. The value of outcomes available ranged from £1.3 million to £2.9 million depending on the region. In terms of funding, the investment secured under their individual SIB arrangements ranged from £310,00 to over £1 million.

Local authorities played a key role in referring participants through their involvement in local ‘referral gateways’, to avoid the risk of cherry picking and focusing efforts on those most likely to achieve outcomes.

Key outcomes (if applicable) and associated measurements

A total of 1,910 young people were recruited by the seven projects during the Year 1 recruitment period, having been allowed to overrecruit on their initial targets by 10% to allow for drop-out. Of all participants enrolled, 87% entered accommodation, with 62% maintaining it for 18 months. 55% of all participants achieved an entry to education or training outcome. Young people engaging with the FCF were less interested in taking up education and training opportunities than originally anticipated. 33% of participants secured employment, with 19% maintaining full-time employment for 13 weeks and 13% for 26 weeks. This outcome was particularly significant given the multiple barriers faced by the participants.

Project performance overall can be summarised in terms of payment received against the value of the outcomes in the bids. Each project claimed either 100% of the outcome value in their bids or where within 10% of doing so. The evaluation acknowledged that while it was difficult to determine whether the SIB or payment-by-results arrangements were more successful, both mechanisms were influential: payment-by-result incentivised outcome achievement, while SIBs provided financial scrutiny and flexibility, promotion innovation and improved delivery.

It is important to note that the estimated costs, cost savings and social value varied considerably between each individual. The costed case studies carried out analysed the costs and benefits of Fair Chance Fund participation for eight individuals. Five participants achieved cost savings and social value exceeding intervention costs in the final year, while for three, costs outweighed savings.